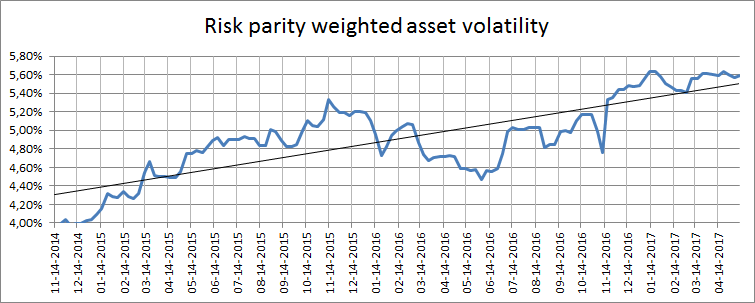

The risk parity weighted asset volatility (the Worldvolatility) stands at 5,59%. This is clearly within the normal range since the early 1970s. The 8th low at around 4% since 1974 occured in 2014 and from this low reading a clear uptrend can be seen until today. This can still be seen as mean reversion and the Worldvolatility have many levels to pass on the upside before it can be said to be high. In other words: -We live in a “normal” world at the moment resembling the late 1990s.