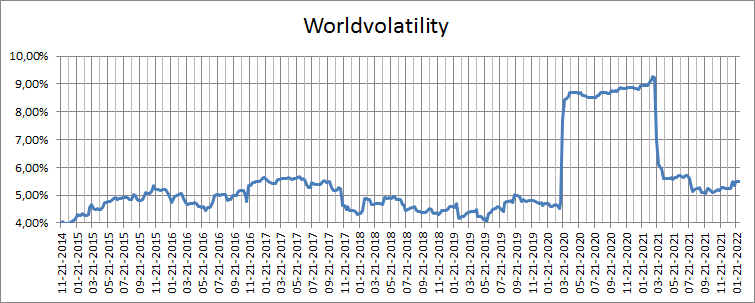

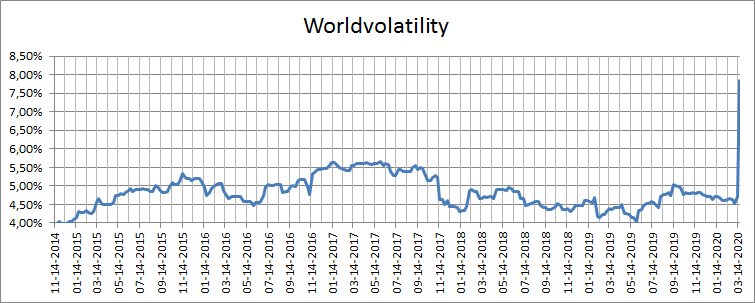

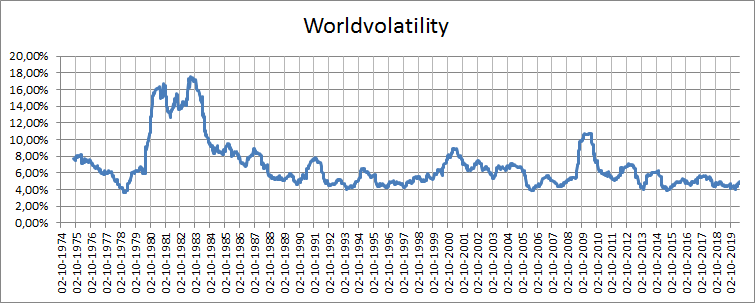

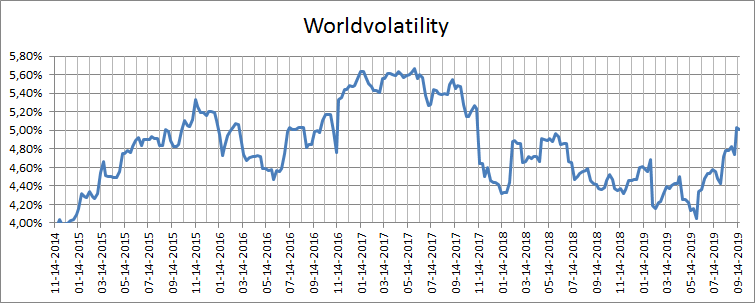

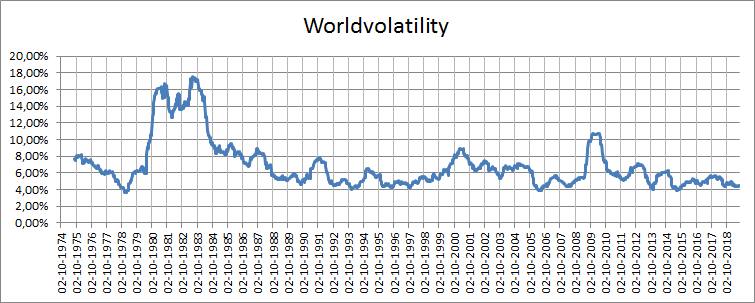

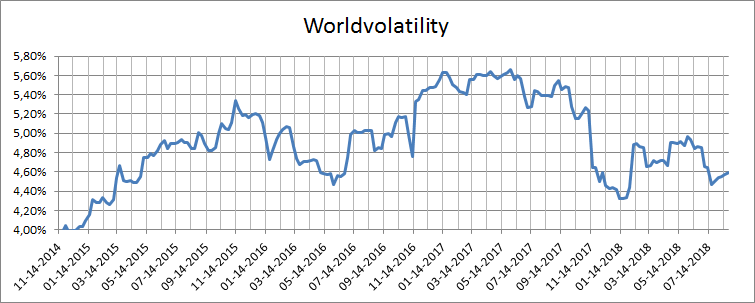

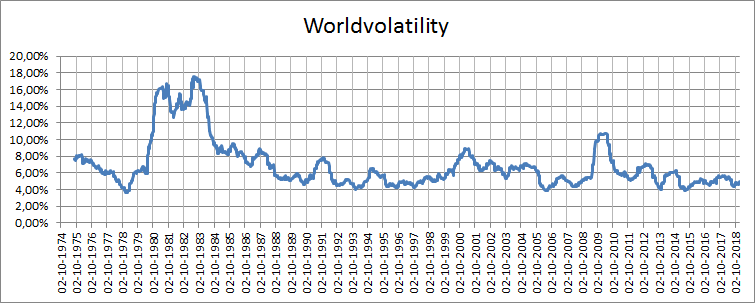

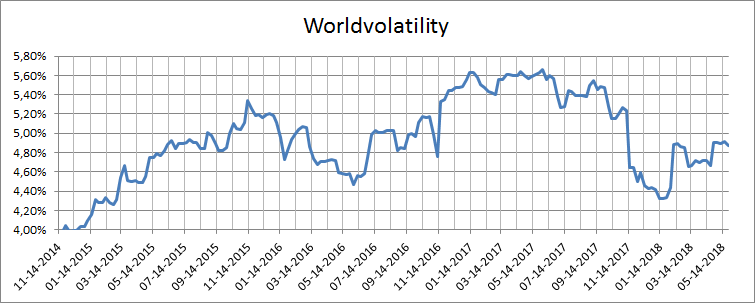

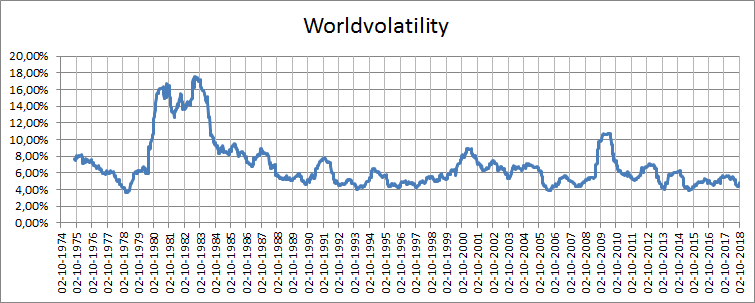

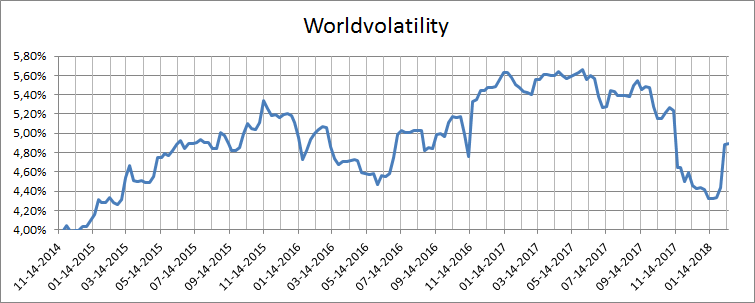

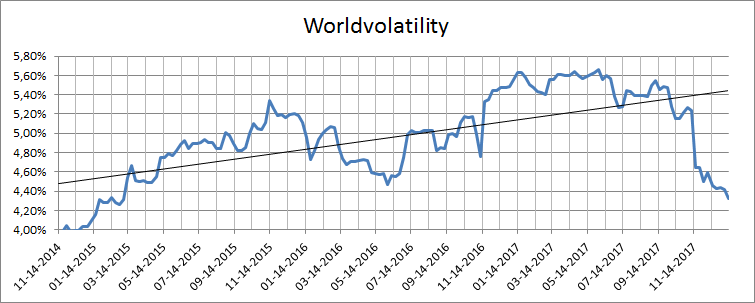

US inflation have reached early 80´s levels for two consecutive months now with energy prices taking the lead. This has lead to a new situation for central bank policies around the world. Monetary tightening is coming but the question is how much and when. BOE were first out with the Fed likely to act in March. The treasury markets are still calm waters but have started a little bit of a selloff. What contributes here is of course way smaller (or none at all) QE buying than in the last couple of years. Equity markets have had a rough start to 2022 but not enough to upset the Worldvolatility.