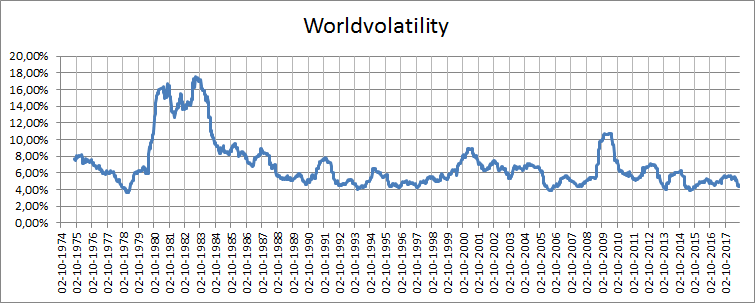

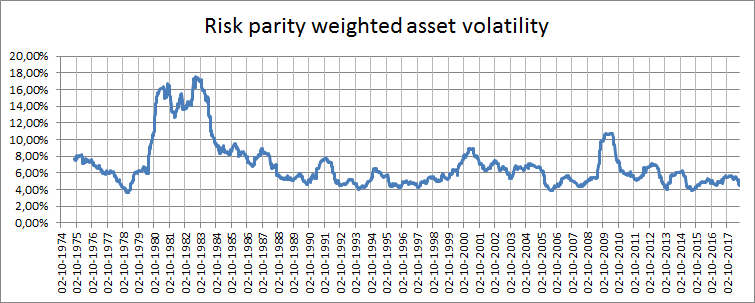

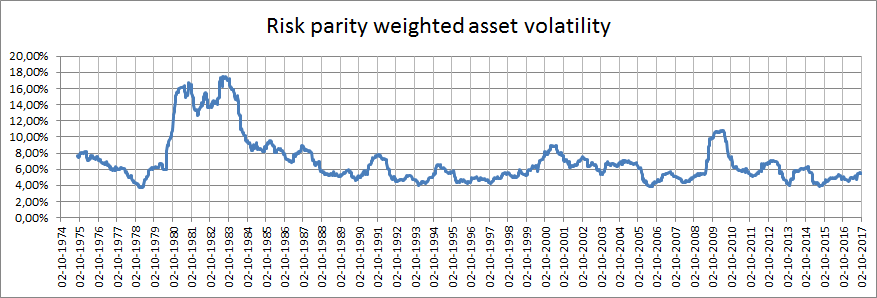

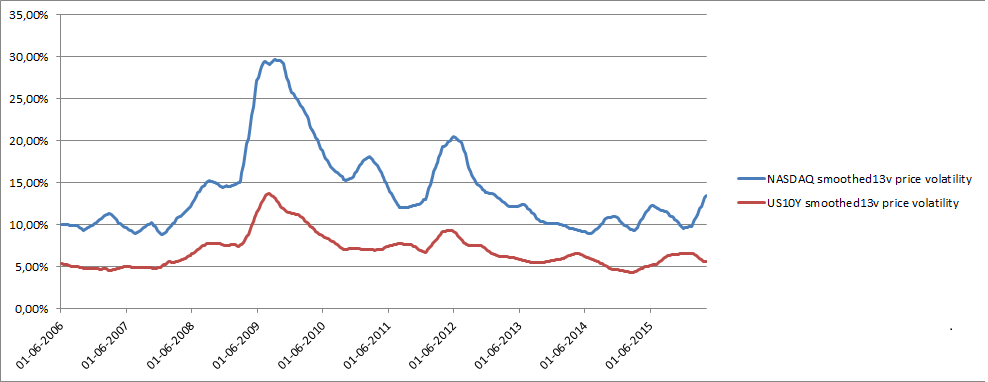

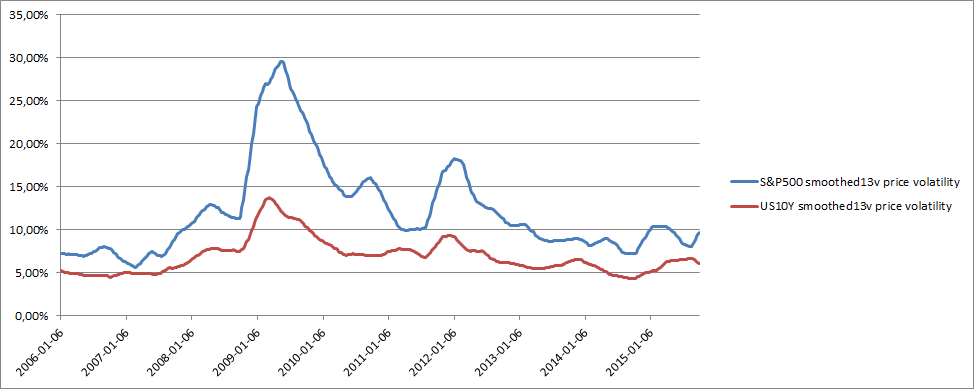

The historic check of Nasdaq and 10year-treasury volatility shows a range of normality for these measures. Treasury volatility seem to be “calm” around 5% and that sets somewhat of a floor. Nasdaq volatility seems to have around 10% as a floor at least in post-coldwar world from the nineties and forward. Upper level obviously harder to pinpoint. Both these series are slightly leptokurtic (fat tail distributed) with Treasuries being more leptokurtic over the 42 year period with only one big spike in volatility.

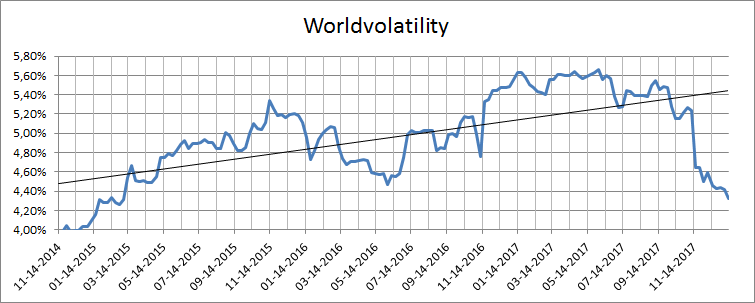

The series looks to be working in “alternating-fashion” in a way with big spikes in one being “safeguarded” by calm in the other. This being brought about by portfolio manager behaviour and central bank behaviour over different periods with different investing fashions in vogue, for example the Volcker-moves of the early eighties by Fed and risk parity investing today.

Is this a reasonable basis for a “worldvolatility”? After researching financial time series and various kinds of societal time series for 20 years my view is that it is.

/Daniel